Interception of Goods in Transit Without Jurisdiction: Allahabad

High Court Orders Immediate Release

By: Adv. (CS) Yogesh Verma / Mob. No. 9571206611

In a significant relief

to taxpayers engaged in interstate trade, the Allahabad High Court has strongly

questioned the powers of State GST authorities in detaining goods merely

passing through the State.

In the case of M/s

J.K. Enterprises vs State of U.P. and Another, the Court observed prima

facie legal mala fides and lack of jurisdiction in the detention of goods

and directed their immediate release.

Background

of the Case

The petitioner, M/s

J.K. Enterprises, was involved in the supply of arecanuts from Guwahati

(Assam) to New Delhi.

During transit:

- The goods were accompanied by valid

documents, including:

- The transaction was clearly an interstate

supply, merely passing through the State of Uttar Pradesh.

However, the goods were

intercepted by GST authorities in Uttar Pradesh on the ground that:

- The tax invoice was signed by an

employee instead of the proprietor.

Verification

of Parties

An important aspect of

the case was that:

- Authorities at Guwahati and New

Delhi independently verified the transaction,

- Both the supplier and recipient

were found to be genuine and bona fide,

Thus, there was no

dispute regarding:

- Genuineness of transaction,

- Validity of documents, or

- Movement of goods.

Issue

Before the Court

The central issue before

the Court was:

👉 Whether State GST authorities can

detain goods in transit during interstate movement on such technical grounds?

Observations

of the Court

The Allahabad High Court

made strong prima facie observations against the department:

1. Lack of Jurisdiction

The Court observed that:

- The goods were in interstate

transit, merely passing through Uttar Pradesh,

- State authorities have limited

jurisdiction in such cases,

Thus, detention of goods

on such grounds appeared to be beyond jurisdiction.

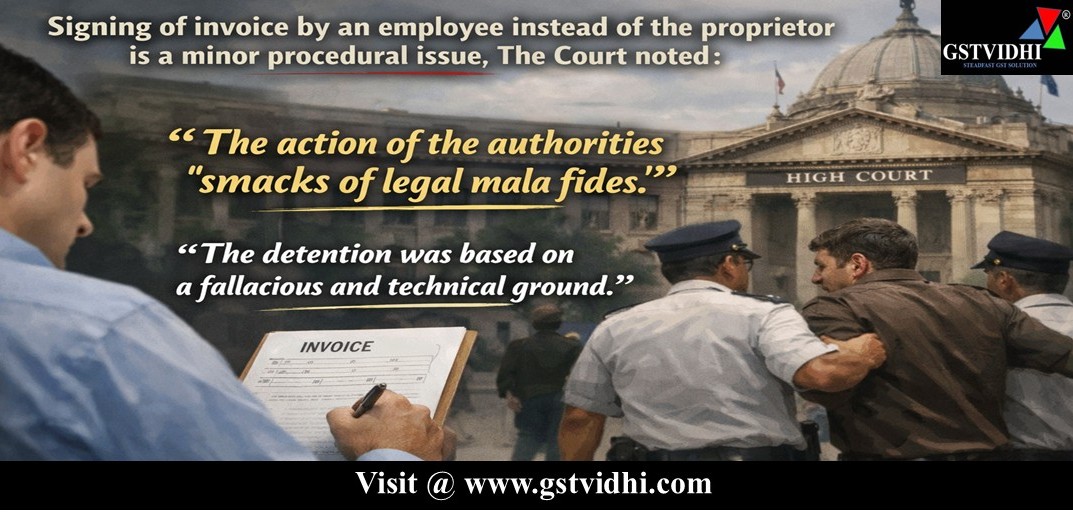

2. Legal Mala Fides

The Court used strong

words, noting that:

- The action of the authorities “smacks

of legal mala fides”,

- The detention was based on a fallacious

and technical ground,

This indicates that the

action was not only incorrect but possibly arbitrary.

3. Technical Lapse Cannot

Justify Detention

The Court noted that:

- Signing of invoice by an employee

instead of the proprietor is a minor procedural issue,

- Such a lapse cannot justify detention

of goods when:

- Transaction is genuine,

- Documents are otherwise valid.

4. Reliance on

Departmental Circular

The Court also took note

of a circular dated 19 January 2021 issued by the State Tax

Commissioner, which governs such situations.

This further strengthened

the view that the action of detention was not in line with departmental

guidelines.

Directions

Issued by the Court

Considering the

seriousness of the matter, the Allahabad High Court passed the following

directions:

- The concerned Assistant Commissioner

was directed to file a personal affidavit explaining the conduct,

- The department was asked to file a

counter affidavit,

- The matter was listed for further

hearing,

Most importantly:

👉 The Court ordered immediate

release of goods, subject to:

- Furnishing of an indemnity bond

equivalent to the security amount under Section 129(1)(a) of the GST

Act.

Conclusion

The judgment in M/s

J.K. Enterprises is a strong reminder that GST enforcement cannot be

mechanical or excessive, particularly in cases of genuine interstate trade.

By ordering immediate release of goods and questioning the authority of

officers, the Allahabad High Court has reinforced that procedural lapses

cannot override substantive compliance. This decision will serve as a

powerful precedent for taxpayers facing similar issues of unjustified

detention during transit.

Disclaimer: All the Information is based on the notification, circular advisory and order issued by the Govt. authority and judgement delivered by the court or the authority information is strictly for educational purposes and on the basis of our best understanding of laws & not binding on anyone.

Click here